A credit card can be effectively free to use — or quietly expensive — depending on how well you understand its fees. Indian card issuers earn from several charges, and most of them are avoidable if you know the rules. This guide breaks down every common fee, when it applies, and how to keep it at zero.

The two fees that actually hurt

Finance charges (interest) and cash-advance fees are the expensive traps — and both are entirely avoidable. Almost everything else is small or waivable.

Joining and annual fees

The two most visible charges are the joining fee (one-time, charged when the card is issued) and the annual fee (recurring, usually charged each year on the card anniversary).

- Many entry-level cards are lifetime-free, with no joining or annual fee at all.

- Mid and premium cards charge an annual fee in exchange for richer rewards, lounge access, or vouchers.

- Crucially, many cards waive the annual fee if your spends in the year cross a set threshold. If you'll comfortably hit that spend anyway, the effective cost is zero.

Always check the waiver condition before judging a fee. A card with a fee that's waived on reasonable spending can be far better value than a "free" card with weak rewards.

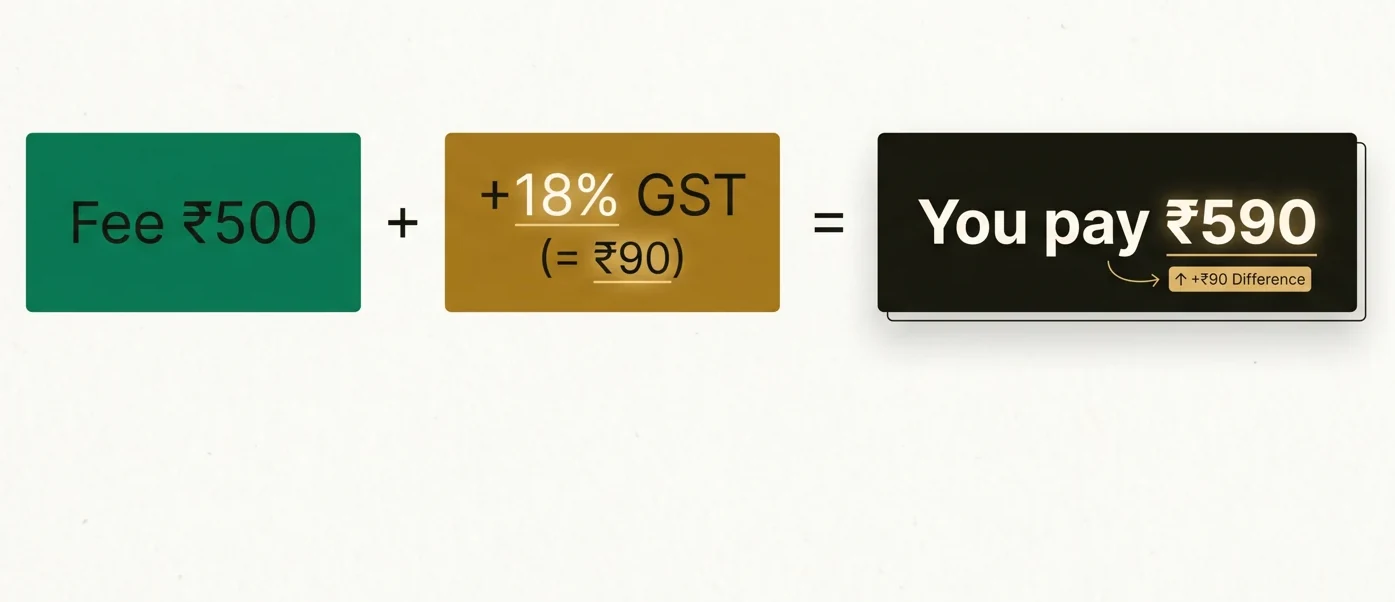

GST on fees and charges

Almost every fee on your credit card attracts 18% GST. This applies to joining and annual fees, interest charges, late payment fees, forex markup, cash advance fees and more.

So a quoted ₹500 annual fee actually costs ₹590 with GST. When you compare cards, mentally add 18% to every charge so you're comparing the true out-of-pocket cost. The GST is set by tax rules, not the bank, so it's identical across issuers.

Forex markup (foreign currency markup)

When you spend in a foreign currency — on an overseas trip or on an international website — the bank converts the amount and adds a forex markup, typically in the range of about 2% to 3.5% of the transaction, plus GST on the markup.

- This applies even to online purchases in dollars or euros from your living room.

- Some travel-focused cards offer a reduced or zero forex markup, which can save serious money if you spend abroad often.

- Separately, large foreign spends may attract TCS (Tax Collected at Source) under the Liberalised Remittance Scheme above an annual threshold — though TCS is adjustable against your income tax, not a permanent loss.

If you travel internationally, the forex markup often matters more than the reward rate.

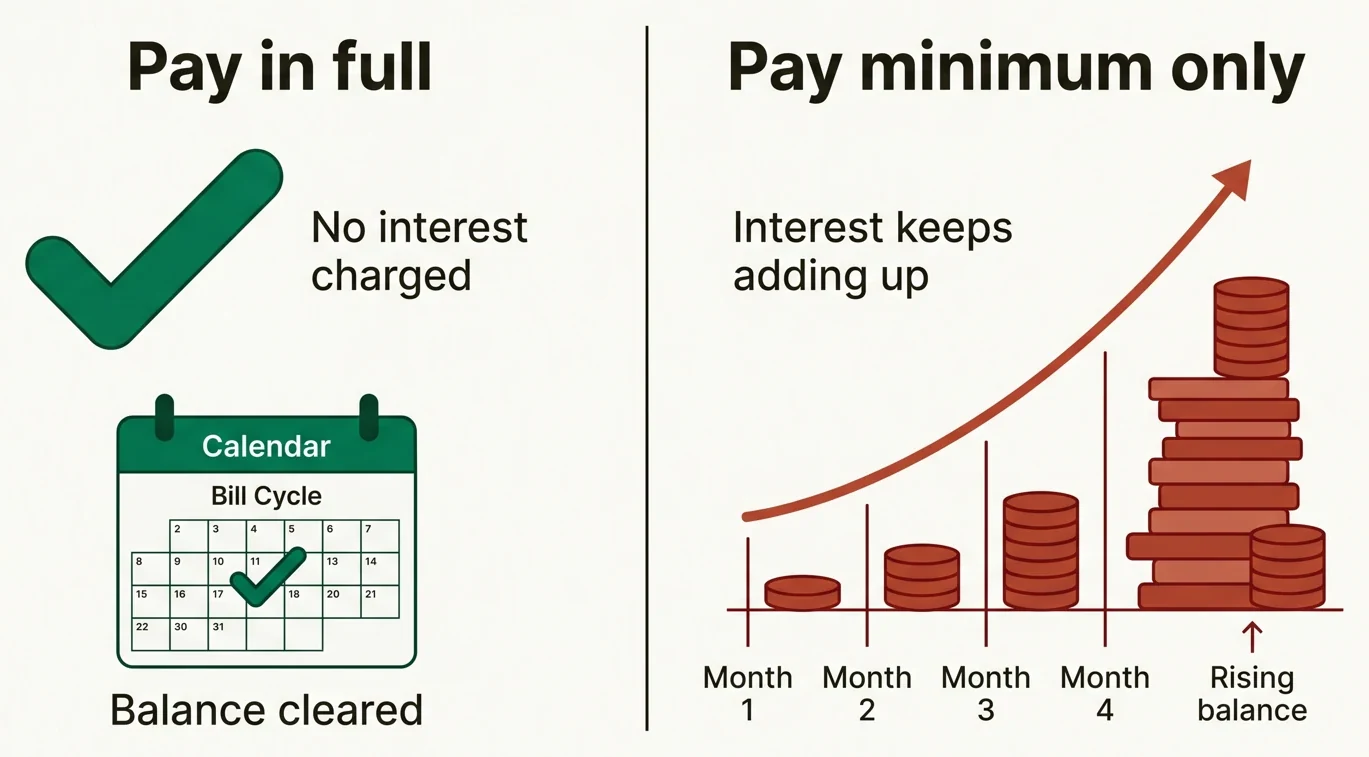

Finance charges (interest)

This is the big one. If you don't pay your full statement balance by the due date, the unpaid amount starts accruing finance charges — interest typically in the range of 3% to 3.75% per month, which works out to roughly 36–45% per year, plus GST.

Two things make this worse than it looks:

- Paying only the minimum due stops late fees but does not stop interest. The remaining balance keeps accruing.

- Once you revolve a balance, you usually lose the interest-free grace period on new purchases too — so fresh spends start charging interest immediately until you clear everything.

The fix is simple: pay the full statement balance, every month, on time. Used this way, your card charges no interest at all.

Fuel surcharge

When you pay for fuel with a credit card, petrol pumps add a fuel surcharge (commonly around 1% of the transaction). Many cards offer a fuel surcharge waiver, often within a monthly cap and a per-transaction range.

- The waiver is usually credited back, not deducted upfront.

- It typically applies only within a transaction-value band, so very small or very large fuel spends may not qualify.

If you drive regularly, a card with a generous fuel surcharge waiver pays for itself.

Cash advance fee

Withdrawing cash from an ATM using your credit card is one of the most expensive things you can do:

- A cash advance fee (often around 2.5–3% of the amount, subject to a minimum) is charged.

- There is no interest-free period — interest starts from the day of withdrawal.

- GST applies on top.

Treat the credit card cash withdrawal feature as an emergency-only option, and clear it the moment you can.

Other fees to watch

| Fee | When it applies | How to avoid |

|---|---|---|

| Late payment fee | Missing the due date | Auto-debit / reminders |

| Over-limit fee | Spending past your limit | Track your balance |

| Reward redemption fee | Some catalogue redemptions | Choose cashback/statement credit |

| EMI processing fee | Converting spends to EMI | Read terms before converting |

| Card replacement fee | Lost/damaged card | Keep the card safe |

| Cheque/payment return fee | Bounced payment | Ensure funds before auto-debit |

All of these attract 18% GST as well.

How to keep your card effectively free

Most cardholders can pay almost nothing in fees by following a few rules:

- Pay the statement in full and on time — this alone eliminates finance charges and late fees, the two biggest costs.

- Pick a card whose annual fee is waived at a spend level you'll naturally reach, or go lifetime-free.

- Never use the card for ATM cash unless it's a genuine emergency.

- Use a low-forex card abroad if you travel, and avoid surprise international online charges.

- Track your due date and limit so over-limit and late fees never trigger.

To see whether a card's annual fee is justified by its rewards, run your real spends through BestCredit's rewards calculator (/recommend) — it shows the net value after fees and GST. You can also check typical reward redemption rates on the point-value page (/points-value).

The bottom line

Credit card fees in India are mostly optional. Finance charges and cash advances are the expensive traps, and both are entirely avoidable by paying in full and never withdrawing cash. Add 18% GST to every quoted charge when comparing cards, prefer a waivable or zero annual fee, and watch the forex markup if you spend abroad. Used with discipline, a credit card costs you nothing while earning rewards and building your credit.