Your CIBIL score is the number lenders look at first when you apply for a credit card or loan. A strong score gets you approved faster, at better interest rates and higher limits. A weak one means rejections or costly terms. The good news: the score is built on a few clear factors you can control. This guide explains how it works and exactly how to improve it.

What a CIBIL score is

CIBIL (TransUnion CIBIL) is one of India's credit bureaus, alongside Experian, Equifax and CRIF High Mark. Each maintains a credit report on you and calculates a three-digit credit score, usually ranging from 300 to 900.

The score is a summary of how reliably you've repaid borrowed money in the past. Lenders pull it (along with your full report) to judge how risky it is to lend to you. Because banks report your repayment data to these bureaus every month, your score updates continuously.

What counts as a good score

While each lender sets its own cut-offs, a common rule of thumb:

| Score range | How lenders generally view it |

|---|---|

| 750–900 | Strong — easy approvals, best rates |

| 700–749 | Good — usually approved |

| 650–699 | Fair — approvals possible, weaker terms |

| 550–649 | Poor — frequent rejections |

| 300–549 | Very poor — hard to get credit |

| NA / NH | No history yet — no score to assess |

If you've never borrowed, you may see "NA" or "NH" instead of a number. That's not bad — it just means there's no track record yet. Getting an entry-level or secured card and using it well creates that record.

How the score is calculated

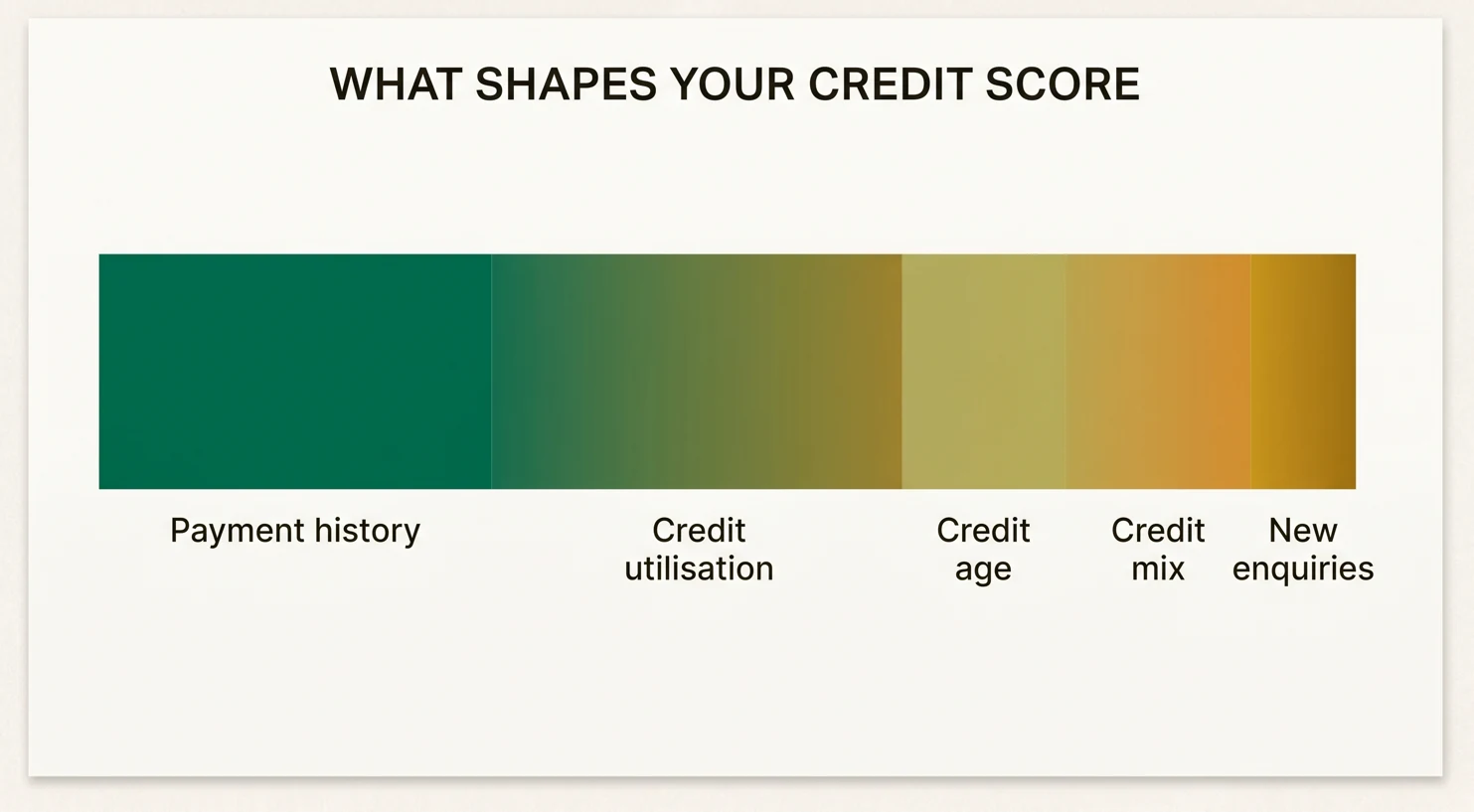

The bureaus don't publish an exact formula, but the broad drivers are well understood. Roughly in order of importance:

- Payment history — whether you pay on time. This is the single biggest factor. Even one missed or late payment can hurt.

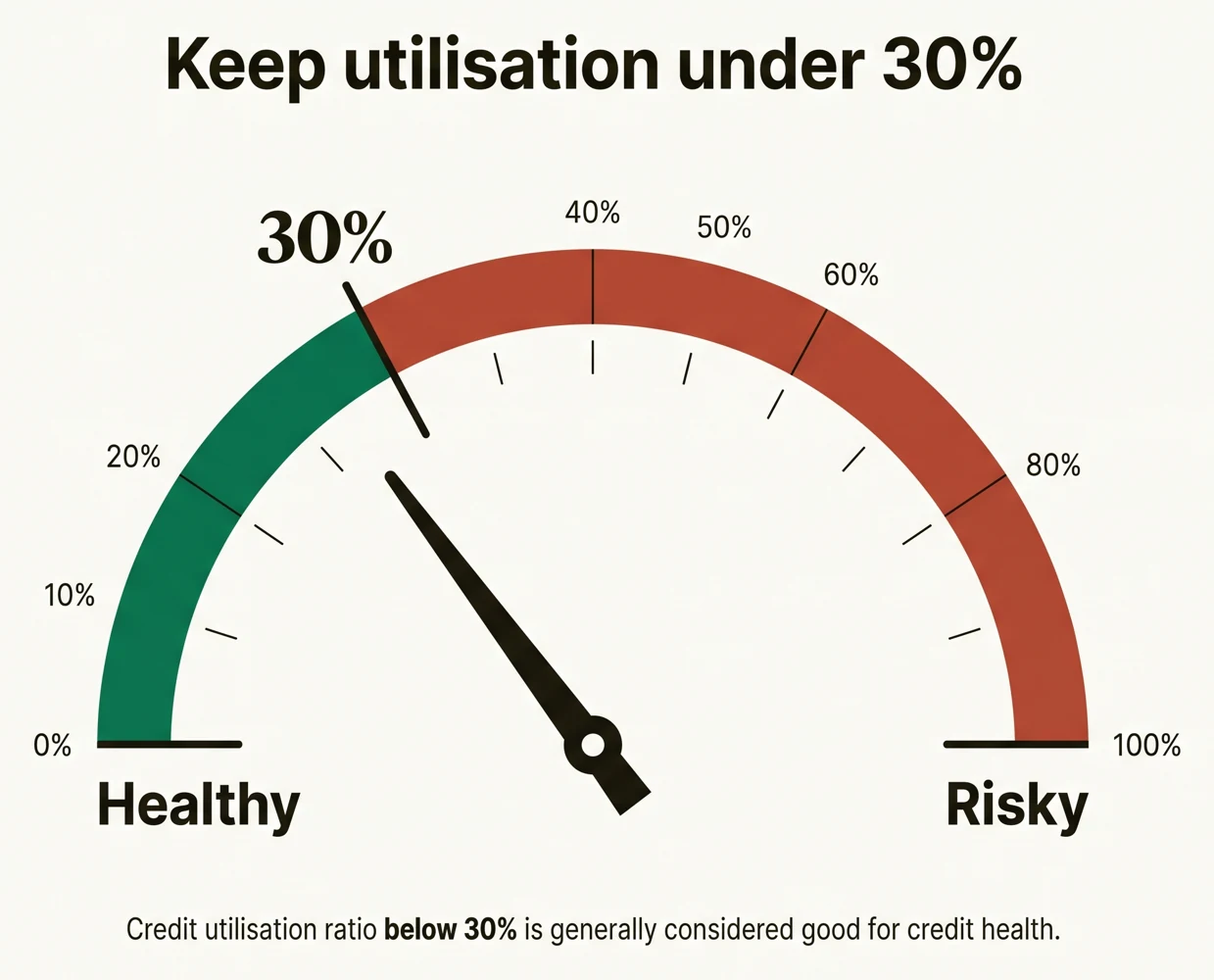

- Credit utilisation — how much of your available limit you use. Lower is better; staying under about 30% helps.

- Credit age and mix — a longer history and a healthy mix of secured (loans) and unsecured (cards) credit looks good.

- New credit and enquiries — applying for many cards or loans in a short period triggers multiple "hard enquiries," which can dent your score.

The two you control most directly day to day are payment history and utilisation.

Why your score might be low

Common reasons people see a weak or stuck score:

- Late or missed payments, including paying only the minimum repeatedly.

- High utilisation — maxing out cards even if you pay them off.

- Too many recent applications in a short window.

- A default or settled account in your history.

- Errors in your report, such as a loan you closed still showing as active, or an account that isn't yours.

- A thin file — too little credit history to judge.

How to improve your CIBIL score

Improvement is gradual but reliable if you stick to these habits:

1. Pay every bill in full and on time

This matters more than anything else. Set up auto-debit for at least the minimum (ideally the full amount) so a forgotten due date never damages your record. Months of on-time payments steadily lift your score.

2. Keep utilisation low

If your limit is ₹1,00,000, try to keep your reported balance under ₹30,000. If you naturally spend more, you can:

- Make a part-payment before the statement is generated, or

- Ask your bank for a limit increase (which lowers your utilisation ratio without you spending less).

3. Don't apply for too much credit at once

Each application can create a hard enquiry. Space out applications, and only apply for cards you're likely to qualify for. Checking your own score (a "soft enquiry") does not hurt it.

4. Keep old accounts open

A long credit history helps. Closing your oldest card can shorten your average credit age and reduce total available limit — so think twice before shutting a no-fee card you've held for years.

5. Maintain a healthy credit mix

A blend of credit types — say a card plus a loan repaid on time — can look better than a single product. Don't borrow unnecessarily just for this, but don't avoid all credit either.

6. Check your report and dispute errors

You're entitled to access your credit report from the bureaus. Review it for mistakes — wrongly reported defaults, closed accounts shown as open, or accounts you don't recognise (a possible fraud sign). Raise a dispute with the bureau to get genuine errors corrected, which can lift your score.

7. Be patient and consistent

There's no instant fix. Negative marks fade and positive history accumulates over months. A consistent six-to-twelve-month run of clean behaviour produces real, lasting improvement.

What does not affect your score

Some common worries are unfounded:

- Checking your own score is a soft enquiry and never lowers it.

- Your income, savings or investments are not part of the score (though lenders consider income separately).

- Debit card usage doesn't build credit history, because there's no borrowing involved.

The bottom line

Your CIBIL score is a running report card of how reliably you repay credit. The fastest way to a strong score is boringly simple: pay in full and on time, keep your card utilisation low, don't chase too many products at once, and keep good old accounts open. Check your report regularly and fix any errors. Build these habits and a score above 750 — and the better cards and loan rates that come with it — is well within reach.