Every rewards credit card in India falls broadly into one of two camps: cashback or reward points. Both give you something back on your spending, but they suit different people. This guide compares them head to head so you can pick the type that actually fits how you spend — and avoid leaving value on the table.

The core difference

- Cashback returns a percentage of your spend as money — credited to your statement or, on some cards, your bank account. ₹100 of cashback is simply ₹100 off your bill.

- Reward points earn you points per spend, which you later redeem for vouchers, travel, statement credit, or merchandise. The value of a point depends entirely on how you redeem it.

In short: cashback is fixed and simple, points are variable and flexible.

Cashback: the case for simplicity

Cashback's biggest strength is that there's nothing to figure out. You know exactly what you're getting, and it directly reduces what you owe.

Pros

- Predictable value — a rupee is a rupee, no conversion maths.

- No expiry games in most cases (though some cards cap or window the cashback).

- No catalogue to navigate or points to "redeem well."

- Works for everyone, regardless of whether you travel or shop online.

Cons

- Caps are common — bonus cashback categories usually have monthly limits.

- The ceiling on value is lower; you rarely beat the headline rate.

- Some cards credit cashback as statement credit only, not real cash.

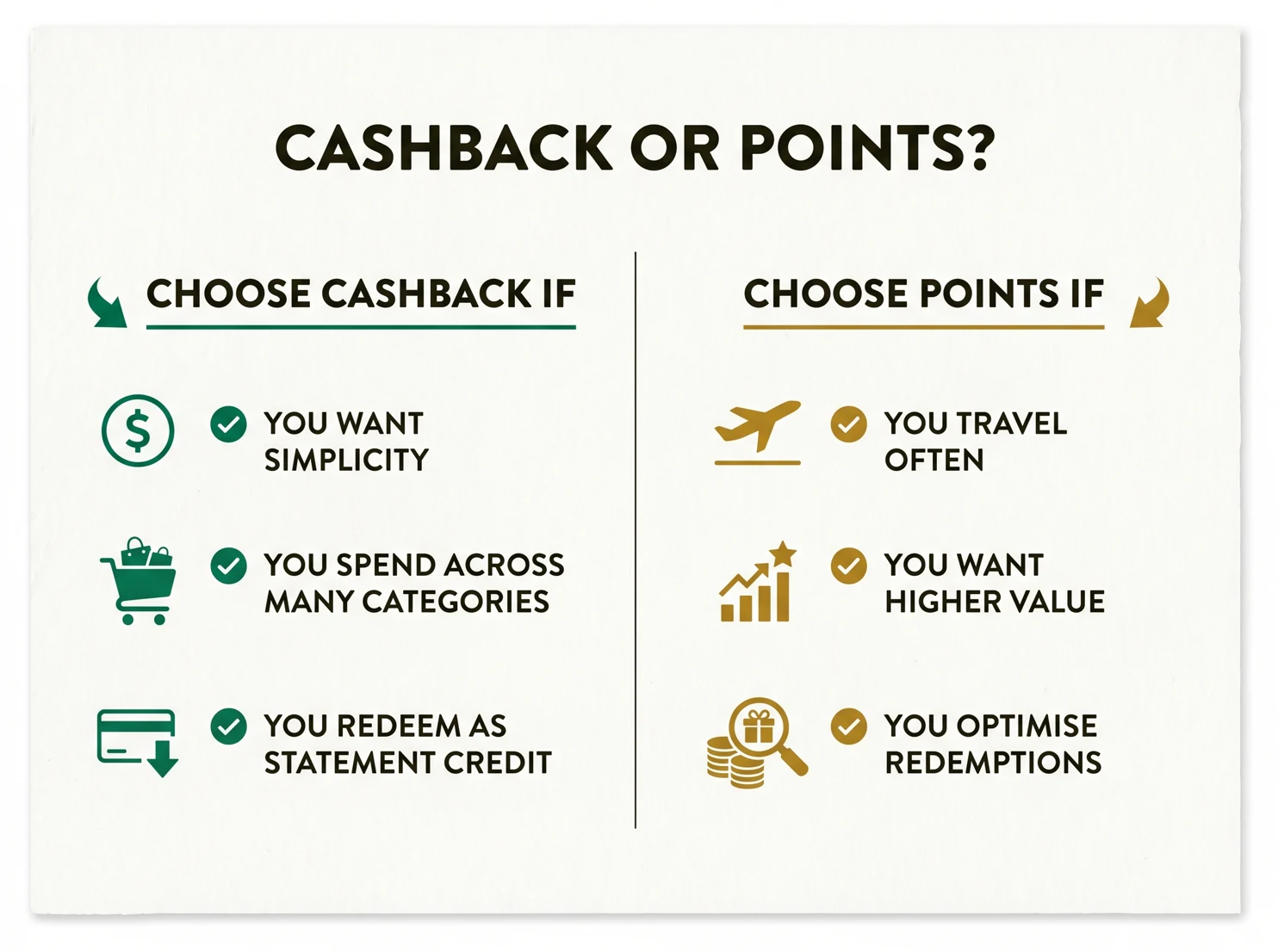

Cashback is ideal if you want maximum simplicity, spend across mixed everyday categories, and don't want to think about redemption.

Reward points: the case for flexibility and upside

Points are more work, but they can be worth more — especially for travellers.

Pros

- Higher upside. Redeemed well (e.g. transferred to airline partners or used via a reward portal), points can be worth more per rupee than flat cashback.

- Flexibility — choose travel, vouchers, statement credit, or transfers depending on what you value.

- Milestone and accelerator benefits are often richer on points cards.

Cons

- Value is variable. The same point can be worth a lot or a little depending on redemption.

- Caps, expiry and redemption fees can erode value if you're not attentive.

- Effort required — you have to track and redeem smartly to win.

Points suit people who travel, spend heavily in bonus categories, and are willing to manage redemptions for extra value.

A side-by-side view

| Factor | Cashback | Reward points |

|---|---|---|

| Value certainty | High (fixed) | Variable |

| Simplicity | Very simple | Needs effort |

| Maximum upside | Moderate | Higher (if redeemed well) |

| Best for | Everyday mixed spends | Travel, heavy category spends |

| Expiry risk | Usually low | Often present |

| Redemption hassle | None | Some |

How to decide for yourself

Ask three questions:

1. Do you travel?

If you fly even a few times a year, points cards that transfer to airline or hotel partners — or book travel through issuer portals — can deliver clearly more value than cashback. If you don't travel, that upside is wasted, and cashback's certainty wins.

2. How much effort will you put in?

Be honest. Points only beat cashback if you redeem them well and avoid expiry. If you know you'll forget about your points or default to the merchandise catalogue (usually the worst value), cashback's "set and forget" nature will likely earn you more in practice.

3. What's your real reward rate after redemption?

This is the deciding number. Convert a points card's earning into an effective cashback-equivalent rate using realistic redemption values, then compare it to a straightforward cashback card. Don't compare a "5X points" claim to "2% cashback" directly — translate points into rupees first. BestCredit's point-value page (/points-value) gives typical conversion rates, and the recommender (/recommend) lets you plug in your spends and see net value on both card types.

You don't have to choose just one

Many smart users keep both:

- A flat cashback card for groceries, bills and miscellaneous spends where simplicity wins.

- A points card for travel and bonus categories where the upside is real.

Route each spend to whichever earns more, and you get the best of both — predictable cashback on the boring stuff and high-value points where it counts.

Don't let the reward type override the fundamentals

Whatever you choose, the rules that protect your money are the same:

- Pay in full every month. Any interest from revolving a balance instantly wipes out cashback or points.

- Mind the annual fee plus GST — the rewards must clearly exceed the cost.

- Respect the caps, on both cashback and points.

The bottom line

Neither is universally "better." Cashback wins on simplicity and certainty — perfect if you spend across mixed categories and want zero hassle. Reward points win on flexibility and upside — ideal if you travel or spend heavily in bonus categories and will redeem with care. Translate any points card into a real rupee value before comparing, use BestCredit's tools to check, and remember that for most people, a cashback card plus a travel-points card together cover every base.