Reward points are the easiest way to get real value back on spending you'd do anyway — but only if you understand how they actually work. Most people leave value on the table by ignoring point values, missing caps and milestones, or redeeming poorly. This guide shows you how to extract the most from Indian credit card rewards without overspending.

First, know what a point is actually worth

A "10X rewards" headline tells you nothing until you know the rupee value of each point. The real metric is:

Reward value = points earned × value per point

A point might be worth anywhere from a fraction of a rupee to over a rupee, depending on how you redeem it. The same points can be worth far more as airline miles than as a catalogue gift, or far less if redeemed as statement credit at a poor rate.

So your first job with any card is to find the effective reward rate — the actual cashback-equivalent percentage after factoring in point value and redemption. BestCredit's point-value page (/points-value) lists typical conversion rates so you can compare cards honestly instead of by marketing claims.

Match cards to spend categories

Most rewards cards pay a base rate on all spends plus accelerated rates on chosen categories — online shopping, dining, travel, groceries, or fuel.

The smart approach is to route each type of spend to the card that rewards it best:

- An online-shopping card for e-commerce.

- A dining/travel card for restaurants and trips.

- A flat-rate card for everything else.

You don't need a wallet full of cards. Even one well-chosen card plus a flat-rate backup covers most people. Use BestCredit's recommender (/recommend) to enter your monthly spend split and see which card or combination earns the most.

Watch the caps — they limit your bonus

Accelerated rewards almost always come with caps. A card may give you boosted points on online spends, but only up to a monthly or statement-cycle limit, after which you drop to the base rate.

To maximise value:

- Know each category's cap and roughly when you'll hit it.

- Once a card's bonus category is "maxed out" for the month, switch that spend to another card.

- Don't chase a bonus you can't fully use — a high headline rate with a tiny cap may earn less than a modest uncapped rate.

Caps are where most people unknowingly lose rewards, so this single habit can meaningfully raise your returns.

Hit the milestones

Many Indian cards offer milestone benefits — bonus points, vouchers, or a fee waiver when your annual or quarterly spends cross set thresholds.

- If you're close to a milestone near the deadline, it can be worth bringing forward a planned purchase to cross it.

- Milestone vouchers (travel, shopping, dining) can be worth more than the points you'd otherwise earn.

- The annual fee waiver is itself a milestone on many cards — reaching the spend threshold makes the card effectively free.

Never overspend just to chase a milestone, but do plan genuine purchases around them.

Use issuer reward portals — carefully

Several banks run dedicated reward and shopping portals that boost earning:

- HDFC SmartBuy and Axis EDGE Rewards / Travel EDGE are well-known examples, where spending through the portal (flights, hotels, gift vouchers) can earn accelerated points or let you redeem points at better rates.

- These portals can multiply value, but read the terms: bonus earning is often capped, and some redemptions carry restrictions or convenience fees.

Treat portals as a tool to amplify spends you were already making, not a reason to spend more.

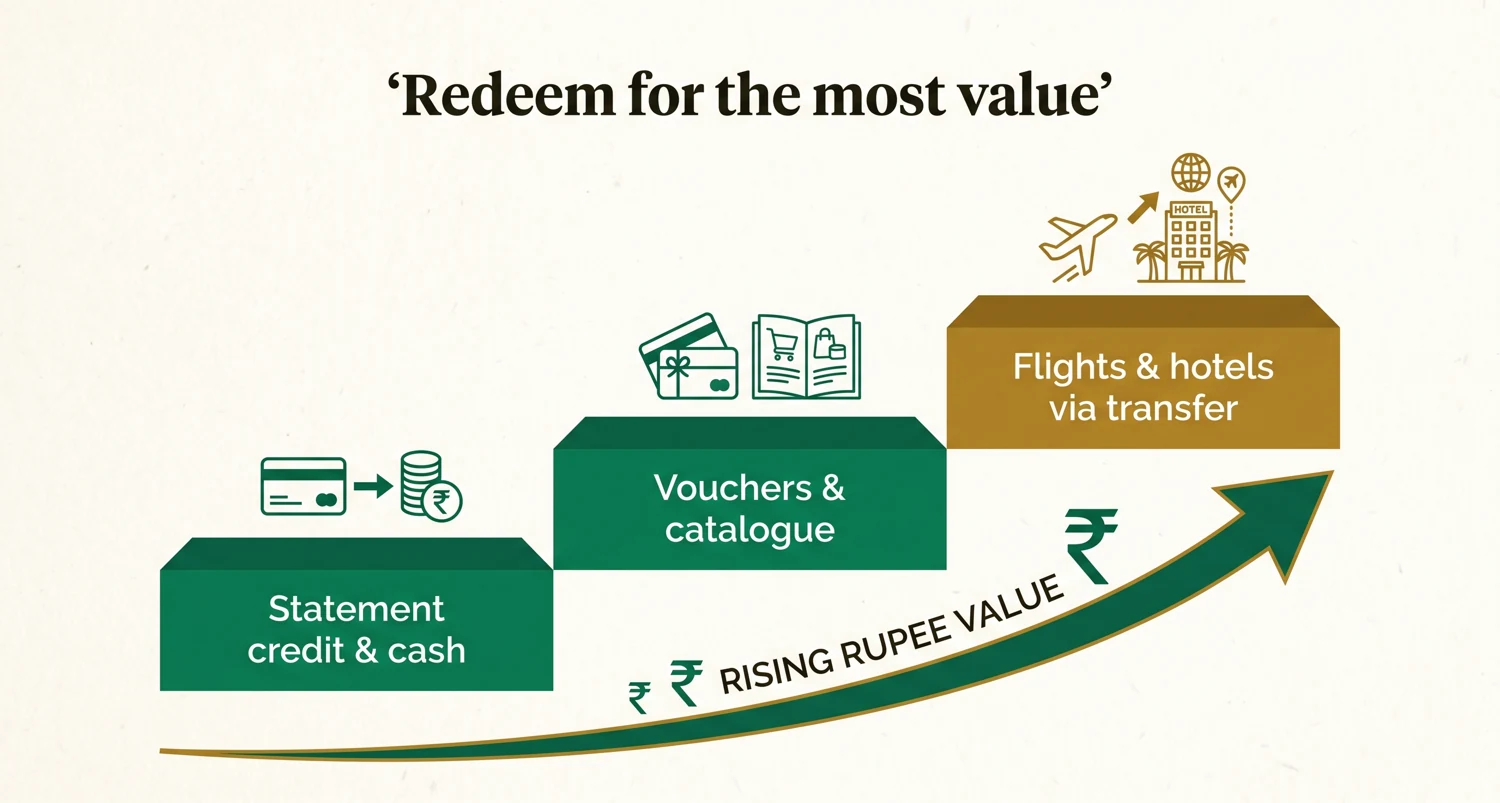

Redeem for maximum value

Where you redeem often matters more than where you earn. As a rough hierarchy:

| Redemption option | Typical value | Notes |

|---|---|---|

| Airline miles / partner transfers | Often highest | Best for travellers; some friction |

| Travel bookings via reward portal | High | Watch for caps |

| Statement credit / cashback | Solid, simple | Easy and predictable |

| Gift vouchers | Moderate | Compare per-point value |

| Merchandise catalogue | Often lowest | Usually poor value |

General principles:

- Avoid the merchandise catalogue unless the per-point value beats your other options.

- Don't let points expire. Many programmes expire points after a set period — redeem before that.

- Check redemption fees, which can quietly eat into value.

- For frequent flyers, transferring to airline partners is often the best-value route, but only if you'll actually use the miles.

Avoid the common traps

- Overspending to earn rewards. If chasing points pushes you to revolve a balance, the interest dwarfs any reward. Always pay in full.

- Ignoring the annual fee. A high-fee card only wins if its rewards clearly exceed the fee plus GST.

- Hoarding points until they devalue or expire. Programmes can change conversion rates; redeem at a steady pace.

- Comparing on headline multipliers instead of effective value. "5X" on a low-value point can be worse than "1X" on a high-value one.

A simple monthly routine

- Route each category to its best card, up to its cap.

- Track progress toward milestones and fee waivers.

- Use issuer portals for big planned spends.

- Pay every statement in full and on time.

- Redeem before expiry, at the highest-value option you'll actually use.

The bottom line

Maximising rewards isn't about spending more — it's about spending smarter. Learn what your points are really worth, send each spend to the card that rewards it best, respect the caps, chase only genuine milestones, and redeem for travel or cashback rather than the catalogue. Run your numbers through BestCredit's recommender (/recommend) and check the point-value page (/points-value) so every comparison is based on real value, not marketing. Do that, and your everyday spending quietly pays you back.