Your first credit card is one of the most useful financial tools you can own — if you pick the right one and use it well. It builds your credit history, gives you a safety buffer for emergencies, and (with the right card) earns you rewards on spends you were going to make anyway. This guide walks you through how to choose wisely, without getting trapped by fees or interest.

Start with why you want a card

Before comparing cards, be clear about your main goal. For most first-time users it falls into one of three buckets:

- Building credit history so you qualify for loans, better cards, and lower interest rates later.

- Convenience and safety — paying online, avoiding carrying cash, and getting fraud protection that debit cards don't always match.

- Rewards — cashback or points on groceries, fuel, dining, or online shopping.

Your goal decides which features matter. If you mostly want to build credit, a simple no-frills card is fine. If you spend heavily online, a rewards card earns its keep.

Check your eligibility first

Indian banks assess you on a few factors before approving a card:

- Income: Most entry-level cards need a modest, stable monthly income. Premium cards demand much higher income.

- CIBIL score: If you've never borrowed, you may have no score yet — that's normal. A score above roughly 750 is considered strong.

- Employment: Salaried applicants are generally approved more easily than self-employed first-timers.

- Age and KYC: You must be 18+ with valid PAN and address proof.

If you have no credit history at all, two beginner-friendly routes exist:

- Secured credit cards issued against a fixed deposit (FD). The bank gives you a card with a limit tied to your FD, so approval is almost guaranteed and you still build credit.

- Entry-level unsecured cards aimed at first jobbers or students from banks where you already hold a salary or savings account.

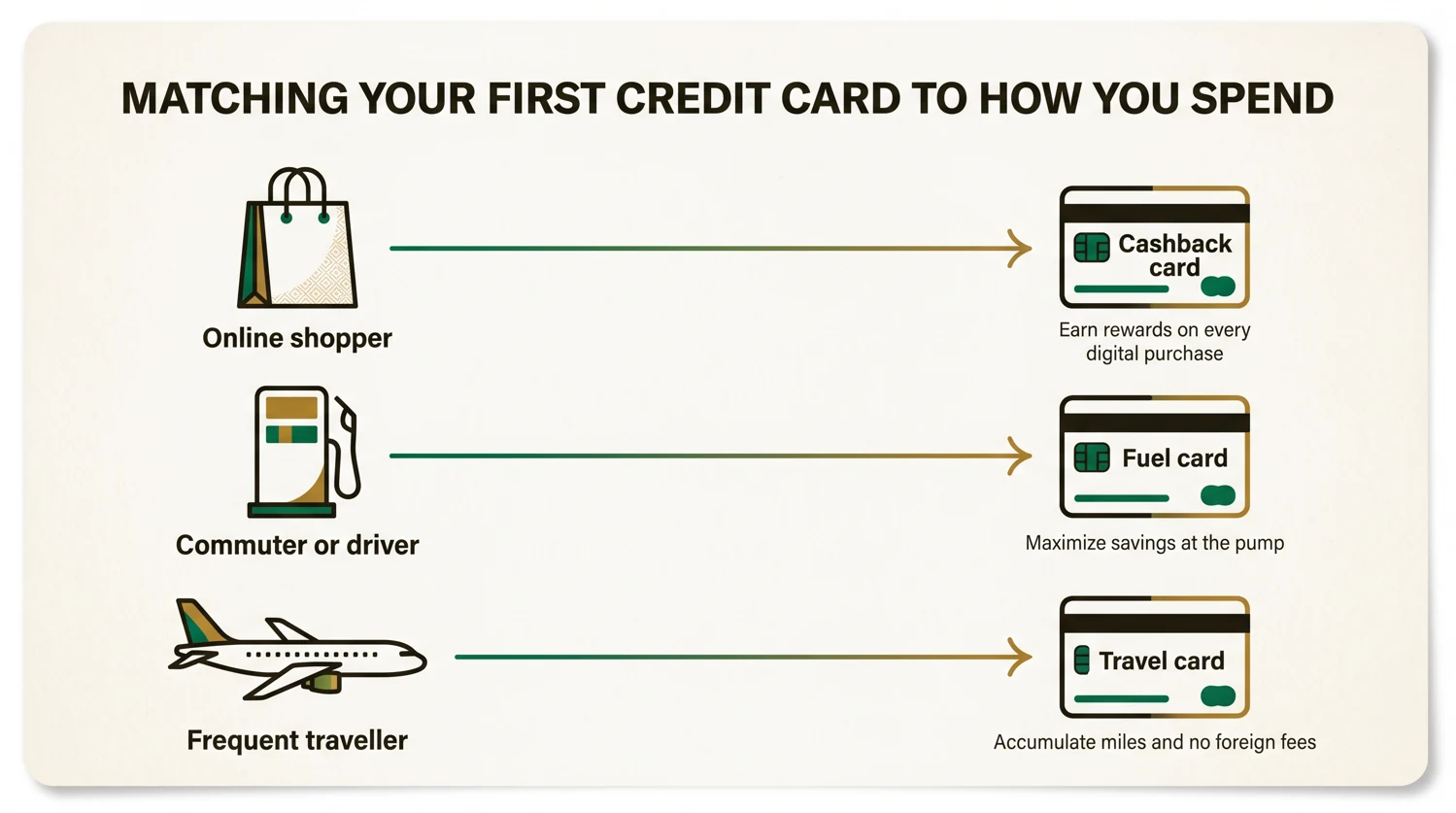

Match the card type to your spending

| Card type | Best for | Watch out for |

|---|---|---|

| Secured (against FD) | No/thin credit history | Limit tied to deposit |

| Basic / lifetime-free | Building credit cheaply | Modest rewards |

| Cashback card | Online and everyday spends | Category caps |

| Fuel card | Heavy fuel users | Limited use elsewhere |

| Co-branded shopping card | Loyal to one retailer/app | Rewards locked to brand |

For a first card, a lifetime-free or low-fee cashback card is usually the sweet spot: no recurring cost, and real value on regular spends.

Weigh the fees honestly

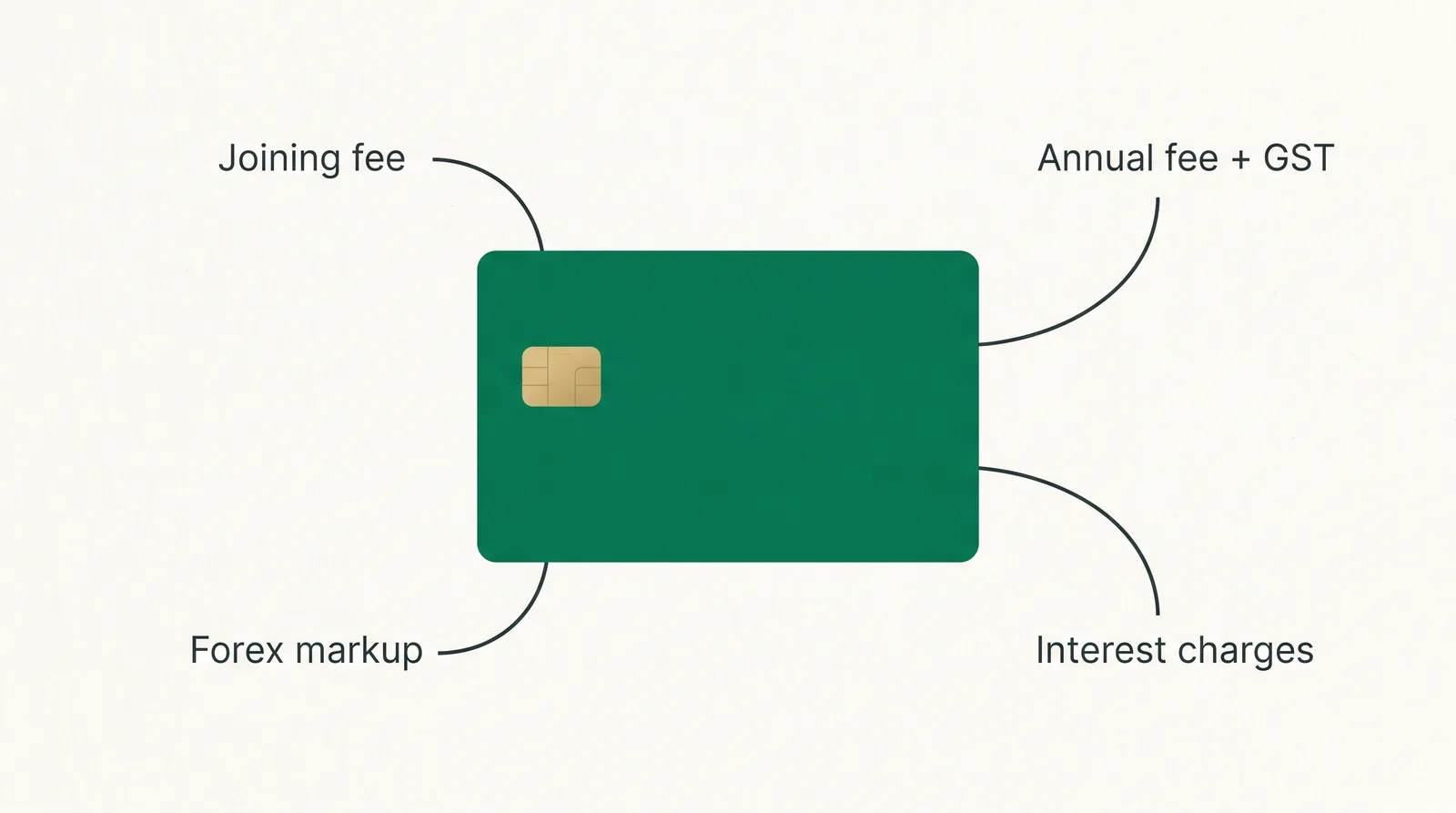

Fees can quietly erase your rewards. Look at:

- Joining and annual fee, and whether the annual fee is waived if you spend above a threshold each year.

- GST — remember that fees and certain charges attract 18% GST.

- Forex markup if you'll ever spend abroad or on international websites (commonly around 2–3.5% plus GST).

- Finance charges — the interest if you don't pay in full. These are high, often in the range of 3–3.75% per month, so never plan to revolve a balance.

- Cash advance fee — withdrawing cash on a credit card is expensive and starts charging interest immediately. Avoid it.

A "free" card with weak rewards can beat a "premium" card whose annual fee outweighs what you earn. BestCredit's rewards calculator (/recommend) lets you plug in your typical monthly spends and see the net value after fees.

Understand rewards before you're dazzled by them

Reward points are only worth what you can redeem them for. A card advertising "10X points" means little until you know each point's rupee value and any redemption restrictions. Check:

- Reward rate in real terms (cashback % or point value per ₹100 spent).

- Caps on bonus categories — many cards cap accelerated rewards monthly.

- Redemption options — statement credit and cashback are simplest; some catalogues offer poor value.

You can look up typical conversion rates on BestCredit's point-value page (/points-value) to compare cards on an apples-to-apples basis.

Useful extras for beginners

Don't pay extra for perks you won't use, but these can add genuine value:

- Fuel surcharge waiver if you drive regularly.

- No-cost EMI on big purchases (read the fine print — processing fees may apply).

- UPI-linked RuPay credit cards, which let you pay via UPI QR codes and often earn rewards on those spends — handy in India's UPI-first economy.

Use your first card the right way

The card matters less than how you use it. Three habits protect your credit and your wallet:

- Pay the full statement balance every month, before the due date. Paying only the minimum keeps you out of default but triggers heavy interest on the rest.

- Keep utilisation low — try to use under 30% of your credit limit. High utilisation can drag down your CIBIL score even if you pay on time.

- Never miss a due date. Set an auto-debit or a reminder. A single missed payment can hurt your score for months.

Over six to twelve months of clean usage, your CIBIL score builds, and you'll qualify for stronger cards and better loan rates.

The bottom line

Pick a card that fits your real spending and charges little or nothing to hold. For most first-timers in India, a lifetime-free or low-fee cashback card — or a secured card if you have no credit history — is the smart starting point. Then use it with discipline: pay in full, stay under your limit, and never miss a date. Compare net value (rewards minus fees) on BestCredit before you apply, and your first card becomes the foundation of a healthy credit profile.