Used correctly, a credit card lets you borrow money for several weeks completely free. Used carelessly, it charges some of the highest interest rates around. The difference comes down to understanding your billing cycle — the statement date, due date, and grace period. Master these and you'll never pay a rupee of interest. This guide explains exactly how it works.

The key dates on your card

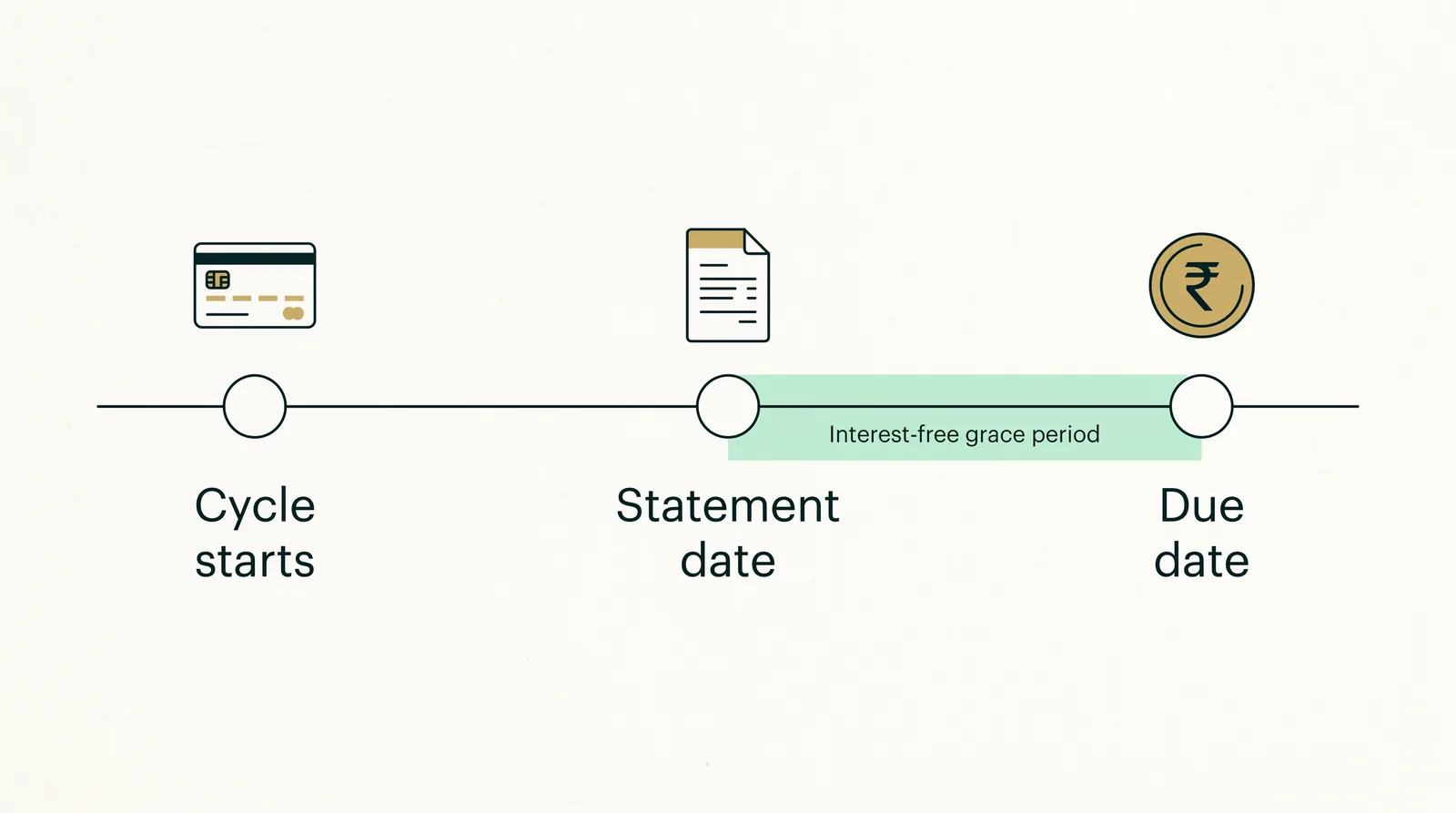

Every credit card runs on a repeating monthly cycle built around four things:

- Billing cycle (statement period): A fixed window, usually about 30 days, during which your spends are recorded. For example, the 6th of one month to the 5th of the next.

- Statement date (billing date): The day the cycle closes and your bill is generated, totalling everything you spent during that period.

- Payment due date: The deadline by which you must pay, usually around 18–21 days after the statement date.

- Grace period (interest-free period): The gap between when you spend and when payment is due — during which no interest is charged, if you pay in full.

How the grace period actually works

The grace period is the secret to free borrowing — but it only applies to new purchases when you pay your full statement balance every month.

Here's the important nuance: the length of your interest-free period depends on when in the cycle you spend.

- A purchase made at the start of the billing cycle enjoys the whole cycle plus the days until the due date — often around 45–50 interest-free days.

- A purchase made just before the statement date gets only the short stretch until the due date — often around 18–21 days.

So the same card can give you anywhere from about 18 to 50 days of free credit, depending on timing. Big planned purchases are cheapest (in cash-flow terms) when made right after a new cycle begins.

A simple worked example

Suppose your billing cycle runs from the 6th to the 5th, your statement is generated on the 5th, and your due date is the 25th.

| You spend on | Appears on statement dated | Due date | Interest-free days |

|---|---|---|---|

| 6th (start of cycle) | 5th next month | 25th | ~50 |

| 25th (mid cycle) | 5th next month | 25th | ~31 |

| 4th (end of cycle) | 5th (next day) | 25th | ~21 |

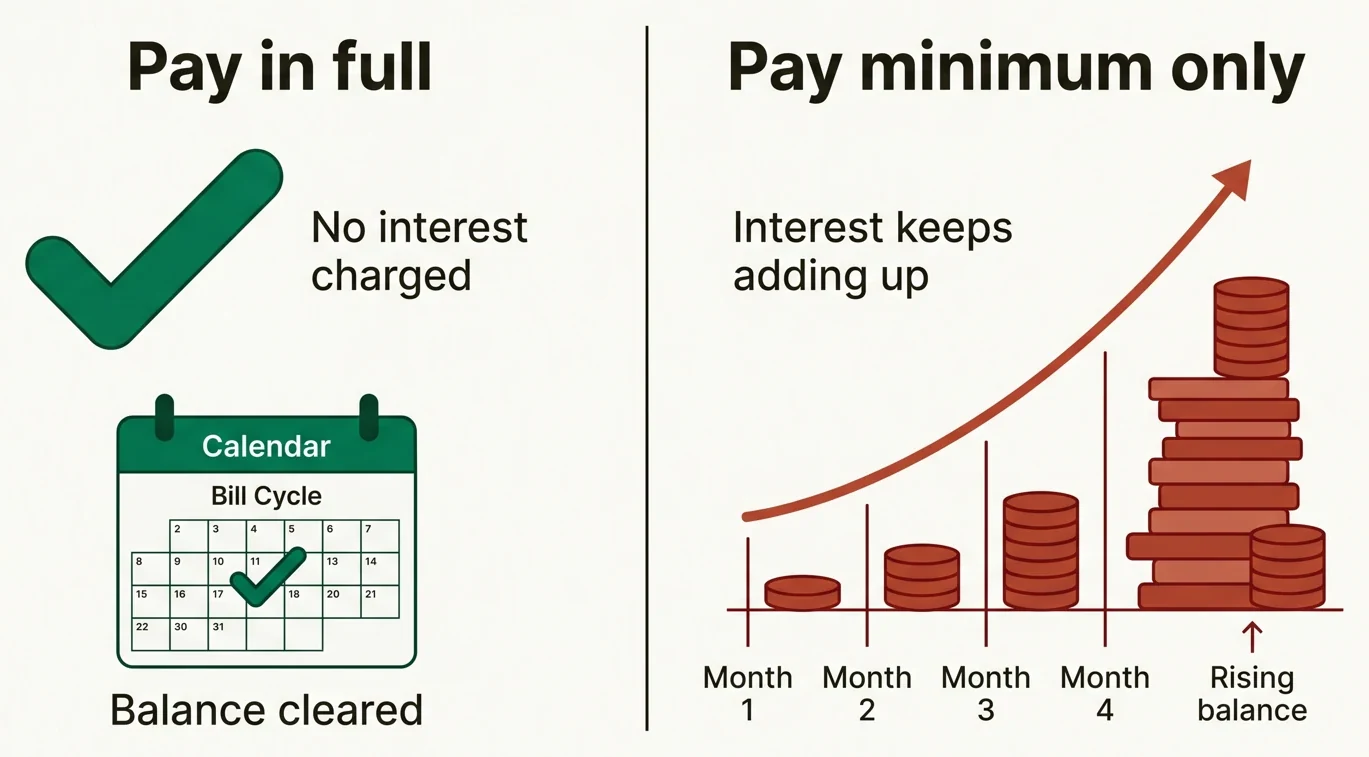

Pay the full statement by the 25th and every one of these purchases costs you nothing in interest.

When interest kicks in — and how badly

If you don't pay the full statement amount by the due date, two expensive things happen:

- Finance charges apply to the unpaid balance — typically around 3% to 3.75% per month, which is roughly 36–45% per year, plus 18% GST.

- You usually lose the grace period on new purchases, too. Once you carry a balance, fresh spends start accruing interest from the transaction date until you clear everything in full.

This is the trap that catches many cardholders, and it's worth restating clearly: paying only the minimum due is not "paying off" your card. It avoids a late fee and a credit-score hit, but the rest of your balance keeps accruing interest, and your new spends do too.

The golden rule: pay the statement balance in full

Avoiding interest is genuinely simple — one habit does it:

Pay your full statement balance by the due date, every single month.

Do this and your grace period stays intact, your new purchases stay interest-free, and your card effectively becomes a free 18-to-50-day loan that also earns rewards.

Statement balance vs total outstanding

Your app may show two figures, which can confuse:

- Statement balance / total amount due: what you owe for the closed billing cycle. Pay this in full to avoid interest.

- Total outstanding / current balance: includes spends made after the statement date, which belong to the next cycle.

You only need to pay the statement balance by the due date to stay interest-free. Paying more is fine but not required.

Cash advances are an exception

The interest-free grace period does not apply to cash withdrawals on a credit card. Interest on cash advances starts from the day you withdraw, on top of a cash advance fee and GST. Treat ATM withdrawals on a credit card as an emergency-only option.

Practical tips to never pay interest

- Set up auto-debit for the full statement amount, not just the minimum, so a missed date can never cost you.

- Know your statement and due dates. Mark them or check your card app.

- Time big purchases for just after a new cycle starts to maximise free credit days.

- Don't revolve a balance. If money is tight, a personal loan or a no-cost EMI is almost always cheaper than carrying a credit card balance at 3%+ a month.

- Avoid cash advances entirely unless it's a true emergency.

- Keep some buffer in your bank account before the due date so the auto-debit doesn't bounce — a returned payment brings its own fee.

What this also does for your CIBIL score

Paying in full and on time isn't just about interest. Payment history is the single biggest factor in your CIBIL score, and keeping your reported balance low helps your utilisation ratio. So the same habit that keeps your card interest-free also steadily strengthens your credit profile — opening the door to better cards and cheaper loans later.

The bottom line

Your billing cycle gives you a built-in interest-free loan of up to roughly 50 days — as long as you pay the full statement balance by the due date every month. Time large purchases just after a new cycle starts, set up a full-amount auto-debit, never revolve a balance, and steer clear of cash advances. Do that, and your credit card costs you zero in interest while earning rewards and quietly building your CIBIL score.